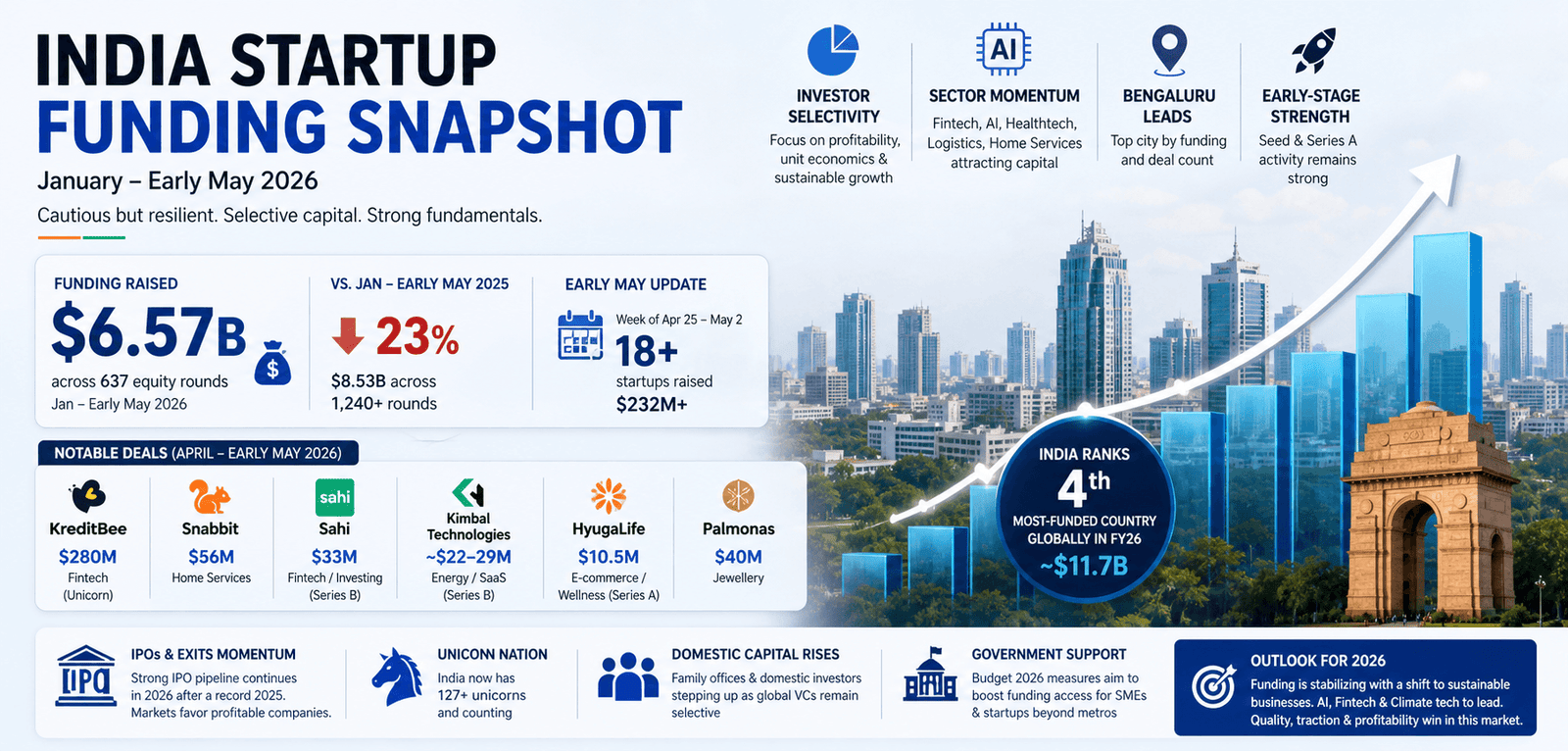

As of early May 2026, India’s startup ecosystem shows a cautious but resilient funding environment. According to Tracxn data (updated May 4, 2026), Indian startups raised $6.57 billion across 637 equity funding rounds from the start of 2026 through early May.

This represents a ~23% decline compared to the same period in 2025 ($8.53 billion across 1,240+ rounds). The slowdown reflects greater investor selectivity, a focus on profitability and unit economics, and fewer mega-deals, though early-stage activity remains steady and sectors like fintech, AI, healthtech, and logistics continue attracting capital.

April 2026 saw $865 million raised (down from $948 million in March), with 92 deals. Only one deal exceeded $100 million. Year-on-year, April improved slightly over 2025 but stayed below 2024 peaks.

Early May data (e.g., the week of April 25–May 2) showed ~18 startups raising over $232 million.

Q1 2026 Context

Q1 provided a stronger start, with reports varying between ~$2.3 billion (Inc42, emphasizing selectivity and no $100M+ deals in some analyses) and higher figures (~$3.9–4 billion in others, boosted by large deals like Neysa’s ~$600M AI infrastructure round). AI funding notably doubled in Q1, though concentrated in a few big bets.

Key Trends in 2026 So Far

- Investor Caution: Emphasis on revenue, profitability, strong fundamentals, and lower cash burn. Late-stage activity has slowed; early- and growth-stage deals dominate volume.

- Sector Highlights:

- Fintech leads (e.g., 42% of April funding).

- Strong interest in AI/deeptech, healthtech, logistics, home services, and consumer/D2C.

- Geography: Bengaluru dominates (e.g., $589M+ or ~68% in April; 89 deals worth $823M in Q1). Delhi-NCR and Mumbai follow.

- Deal Mix: More deals overall in some quarters, but smaller average sizes outside outliers. Seed and Series A remain active.

- Exits & IPOs: Strong IPO pipeline in 2026 following 2025’s record year. Multiple startups have filed DRHPs; public markets favor profitable companies.

Notable Deals (Recent/April–Early May)

- KreditBee (Fintech): $280M (major April deal, unicorn status).

- Snabbit (Home services): $56M.

- Sahi (Fintech/Investing): $33M (Series B).

- Kimbal Technologies (Energy/SaaS): ~$22–29M (Series B).

- HyugaLife (E-commerce/Wellness): ~$10.5M (Series A).

- Palmonas (Jewellery): $40M.

- Others: Polaris ($80M), plus various seed deals in AI, healthtech, and agritech.

Weekly aggregates show consistent smaller rounds in diverse sectors (gaming, edtech, cybersecurity, etc.).

Broader Ecosystem

- India ranks as the 4th most-funded country globally in FY26 (ended March 2026) with ~$11.7B, behind the US, UK, and China.

- Over 674K startups total; ~33.9K funded, with strong unicorn creation (now 127+).

- Domestic capital and family offices increasingly fill gaps as some foreign VCs remain selective.

- Government focus (e.g., Budget 2026 measures for SMEs/MSMEs) aims to support broader access to funding beyond top metros.

Outlook for Rest of 2026

Funding is stabilizing post-2025 adjustments, with a shift from “growth at all costs” to sustainable models. AI, fintech, and climate/sustainability tech are expected to lead. The robust IPO pipeline could provide exits and confidence. Challenges include global macro pressures and valuation realism, but India’s large talent pool, digital infrastructure, and domestic investor base support long-term optimism.

Data Sources: Primarily Tracxn, Inc42, Entrackr, Economic Times, and ecosystem reports (as of early May 2026). Funding figures are approximate and can vary by inclusion of debt/undisclosed rounds.

This monthly snapshot highlights a maturing ecosystem prioritizing quality over quantity. Stay tuned for mid-May updates as more deals close. For founders: traction, profitability, and clear moats are key in this selective market.